Moving to Thailand can cost far less than relocating to many Western countries, but that does not mean it is automatically cheap. The amount you need depends on several factors, including where you plan to live, what visa route you are taking, how comfortable you want your lifestyle to be, and how much of a financial cushion you want behind you.

Some people arrive with just enough for the flight, rental deposit, and a few months of basic expenses. Others prefer to come with a much larger buffer so they can cover visa fees, health insurance, setup costs, and unexpected problems without putting themselves under pressure. The difference is not just budget. It is also about risk.

In this guide, I break down the real cost of moving to Thailand, from one-time relocation expenses to ongoing monthly costs. I also cover healthcare, insurance, emergency savings, and the common budgeting mistakes people make before the move. Toward the end, you’ll also find a relocation budget tool to help you estimate your own numbers more realistically.

Before You Calculate – What Kind of Move Are You Making?

Before you start calculating numbers, it’s worth taking a step back and being clear about what kind of move you are actually planning. This is where many people get their budget wrong, because not every move to Thailand looks the same.

For example, there is a big difference between coming to Thailand for a few months to “try it out” and relocating long-term with the intention to build a life here. The costs, risks, and financial requirements can vary significantly depending on your situation.

✅ Most people fall into one of the following categories:

Short-Term Trial Stay (1–6 Months)

This is often the first step. You come to Thailand to see if the lifestyle suits you before making any long-term commitments.

Your budget can be relatively lean, but you still need to account for:

- flights

- short-term accommodation (often more expensive than long-term rent)

- daily expenses

- a small buffer for flexibility

📌 The biggest mistake here is underestimating how quickly costs add up when you are not settled yet.

Long-Term Relocation

This is a more serious move. You are planning to stay in Thailand for the foreseeable future, whether for lifestyle, work, or a fresh start.

Your budget needs to cover more than just the basics:

- rental deposits and initial setup costs

- visa-related expenses

- health insurance

- a proper financial buffer

📌 This is where planning becomes critical. A tight budget can quickly turn into stress if something does not go as expected.

Retirement in Thailand

If you are moving to Thailand for retirement, your financial planning needs to be more structured.

In addition to living expenses, you should consider:

- visa requirements (financial thresholds)

- long-term healthcare and insurance

- stability of income or savings

- lifestyle expectations over time

📌 Many retirees underestimate healthcare and overestimate how far their budget will stretch long-term.

Digital Nomad or Remote Worker

If your income comes from abroad, your situation is more flexible, but it still requires planning.

You need to think about:

- income stability

- currency fluctuations

- workspace and connectivity

- travel and visa flexibility

📌 The risk here is assuming income will always remain stable. A financial cushion is still essential.

Once you are clear on which category you fall into, it becomes much easier to estimate how much money you actually need. In the next section, I’ll give you a realistic overview of typical budget ranges so you have a clear starting point before we break things down in detail.

Many people think the question is “How much money do I need?”

In reality, the better question is “What kind of move am I making?”

📍 That answer will determine everything else.

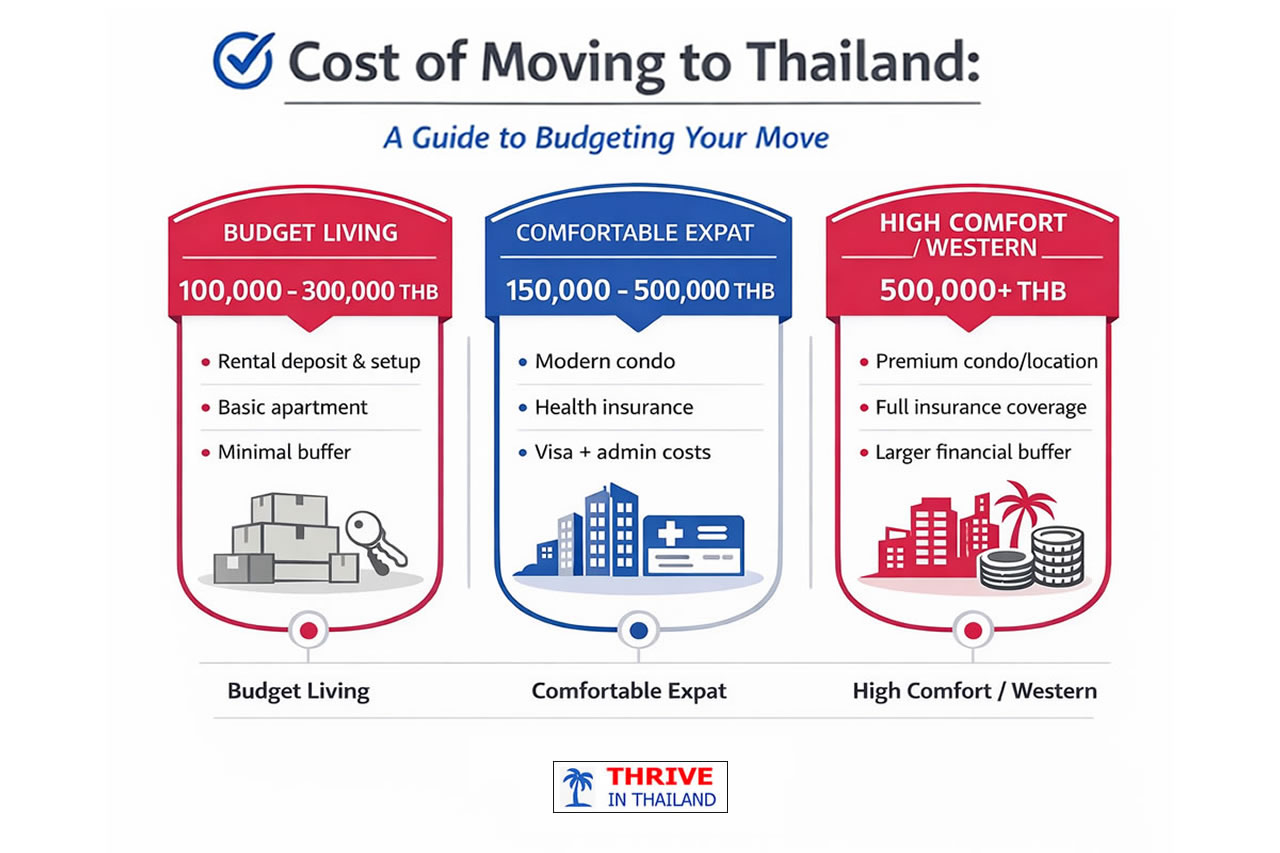

The Short Answer – Realistic Budget Ranges

If you are looking for a quick answer, here is a realistic starting point based on different lifestyles and levels of financial comfort. These are not exact figures, but they give you a solid baseline before we break things down in more detail.

Typical Monthly Costs and Relocation Budget

These ranges reflect what it typically takes to live in Thailand comfortably without unnecessary financial pressure.

| Lifestyle Level | Monthly Budget (THB) | Monthly Budget (USD) | Recommended Relocation Budget (THB) | Recommended Relocation Budget (USD) |

|---|---|---|---|---|

| Basic Living | 35,000 – 50,000 | 1,000 – 1,400 | 150,000 – 250,000 | 4,200 – 7,000 |

| Comfortable Expat | 50,000 – 85,000 | 1,400 – 2,400 | 250,000 – 450,000 | 7,000 – 12,500 |

| High Comfort / Western-Style Living | 85,000 – 180,000+ | 2,400 – 5,000+ | 450,000 – 900,000+ | 12,500 – 25,000+ |

📌 These numbers assume a single person and a relatively standard setup without major luxury spending or extreme cost-cutting.

💱 Currency Note:

All USD estimates are based on an approximate exchange rate of 1 USD = 35 THB.

Actual amounts may vary depending on current exchange rates.

Your actual budget can vary depending on:

- location (Bangkok vs Chiang Mai vs islands)

- accommodation type

- visa situation

- health insurance coverage

- personal lifestyle expectations

✅ Thailand can be affordable, but it is not “cheap” in the way many people expect. The more stability and comfort you want, the more important it becomes to plan realistically and allow for a margin of safety.

What Actually Determines Your Budget

The ranges above give you a general idea, but the actual amount you need can vary quite a bit depending on your situation. Two people living in Thailand can have completely different expenses, even if they are in the same city.

Instead of focusing only on averages, it’s more useful to understand what actually drives your costs. Once you know this, you can adjust your budget based on your own priorities rather than relying on generic estimates.

Location

Where you choose to live has one of the biggest impacts on your budget.

Bangkok, Phuket, and popular beach destinations tend to be more expensive, especially when it comes to rent and daily lifestyle costs. In contrast, places like Chiang Mai or smaller provincial towns can offer significantly lower living expenses while still providing a comfortable lifestyle.

📌 Even within the same city, prices can vary depending on the neighborhood, proximity to public transport, and the type of accommodation you choose.

Accommodation Style

Your housing choice will likely be your largest monthly expense.

A simple studio apartment in a local area will cost far less than a modern condo in a central location with facilities like a pool, gym, and security. Long-term rentals are usually much cheaper than short-term stays, but they often require deposits and upfront payments.

📌 This is also where many newcomers overspend in the beginning by booking something convenient instead of something sustainable.

Lifestyle Expectations

How you live day to day makes a big difference.

Eating local Thai food, using public transport, and keeping entertainment simple can keep your costs low. On the other hand, regularly dining in Western restaurants, using taxis or Grab, and maintaining a more Western lifestyle can increase your monthly budget quickly.

📌 There’s no right or wrong approach here — it simply comes down to what you value and what you are comfortable spending.

Visa Situation

Your visa type can directly and indirectly affect your budget.

Some visas require financial proof or ongoing income, while others involve application fees, extensions, or border runs. Over time, these costs can add up and should be factored into your overall plan. Understanding your visa options is an important part of planning your budget. → Long-Term Visa Options

Health Insurance and Healthcare

This is one of the most commonly underestimated expenses.

While basic healthcare in Thailand can be affordable, more serious treatments or private hospital care can become expensive. Health insurance helps reduce that risk, but premiums vary depending on your age, coverage level, and medical history.

📌 Skipping insurance might seem like a way to save money at first, but it can become a costly mistake later.

Personal Spending Habits

Finally, your individual habits will always play a role.

Some people are naturally more conservative with spending, while others prioritize comfort, convenience, or social activities. Small daily choices can add up over time and significantly influence your monthly budget.

One-Time Relocation Costs

Before your monthly expenses even begin, there are several one-time costs involved in moving to Thailand. These can add up quickly, especially in the first few weeks, and are often underestimated. Understanding these upfront costs is essential, because this is where many people run into financial pressure early on.

Flights

Your first major expense is getting to Thailand.

Flight prices vary depending on your departure location, time of year, and how far in advance you book. Long-haul flights from Europe or North America are typically more expensive, while regional flights within Asia can be significantly cheaper.

📍 Typical range:

- 20,000 – 45,000 THB ($550 – $1,250)

Initial Accommodation

Unless you already have long-term housing arranged, you will likely need temporary accommodation when you arrive.

Hotels, serviced apartments, or short-term rentals are more expensive than long-term leases, but they give you flexibility while you explore different areas.

📍 Typical range (2–4 weeks):

- 10,000 – 40,000 THB ($300 – $1,100)

📌 Staying longer in short-term accommodation is one of the easiest ways to overspend early on.

Rental Deposits and Advance Rent

When you move into a long-term rental, most landlords require:

- 1–2 months deposit

- 1 month rent in advance

For a mid-range condo, this can add up quickly.

📍 Typical range:

- 20,000 – 100,000+ THB ($550 – $2,800+)

Visa Costs

Your visa expenses depend on the type of visa you choose.

This can include:

- application fees

- extension fees

- re-entry permits

- occasional travel costs (if required)

📍 Typical range:

- 2,000 – 20,000+ THB ($55 – $550+)

📌 Some visa routes are inexpensive, while others require more ongoing costs and planning.

Health Insurance Setup

If you plan to stay long-term, health insurance should be part of your initial setup.

Depending on your age and coverage level, you may need to pay upfront or annually.

📍 Typical starting cost:

- 10,000 – 50,000+ THB ($280 – $1,400+)

📌 This is not an area where cutting corners is advisable.

Basic Setup Costs

Even if you move into a furnished place, there are always small setup expenses.

These can include:

- SIM card and mobile data

- basic household items

- transport setup (bike rental, deposits, etc.)

- initial groceries and essentials

📍 Typical range:

- 5,000 – 20,000 THB ($140 – $550)

📌 When you combine these costs, it becomes clear why arriving with only a minimal budget can be risky. Even before your regular monthly expenses begin, you may already need a significant amount just to get settled.

Monthly Costs vs One-Time Costs

When planning your move to Thailand, it’s important to clearly separate your one-time relocation costs from your ongoing monthly expenses.

Your relocation budget covers everything you need to get started, such as flights, deposits, visa fees, and initial setup costs. These are expenses that occur once, usually within the first few weeks after arrival.

Your monthly budget, on the other hand, reflects your day-to-day living costs once you are settled. This includes rent, food, transportation, utilities, insurance, and personal spending.

Keeping these two categories separate helps you avoid a common mistake: arriving with enough money to get started, but not enough to sustain your life here comfortably.

✅ For a more detailed breakdown of ongoing expenses, you can explore typical monthly costs in Thailand.

Location Matters More Than You Think

Where you choose to live in Thailand has a major impact on how far your budget will go. Two people with the same lifestyle can have very different expenses simply based on location.

Bangkok and popular beach destinations like Phuket tend to be the most expensive, especially when it comes to rent, dining, and day-to-day convenience. Condos in central areas or near the beach can quickly push your monthly budget higher, particularly if you prefer modern buildings with good facilities.

In contrast, cities like Chiang Mai or smaller provincial towns offer a much lower cost of living while still providing a comfortable lifestyle. Rent is usually cheaper, daily expenses are lower, and it’s easier to stay within a moderate budget without sacrificing too much comfort.

Even within the same city, prices can vary significantly depending on the neighborhood. Living near public transport, in expat-heavy areas, or in newly developed zones often comes at a premium, while local neighborhoods tend to be more affordable.

As a rough guideline, living in Bangkok or Phuket can cost 20–40% more than living in Chiang Mai or smaller cities, depending on your lifestyle.

📌 Choosing the right location is not just about saving money. It’s about finding a balance between lifestyle, convenience, and long-term sustainability.

Healthcare & Insurance Costs

Healthcare is one of the most important factors to consider when planning your budget for Thailand, yet it’s often overlooked in the early stages.

Thailand has a well-developed healthcare system, and many private hospitals offer a high standard of care at reasonable prices compared to Western countries. For routine treatments and minor issues, costs can be quite manageable even without insurance.

However, more serious medical situations can become expensive, especially if you require hospitalization, surgery, or ongoing treatment. This is where many people underestimate the financial risk.

Health insurance helps reduce that uncertainty, but it comes at a cost. Premiums vary depending on your age, the level of coverage you choose, and whether you want local or international protection.

For younger expats, basic plans can be relatively affordable. As you get older, premiums increase, and coverage options may become more limited. This makes long-term planning particularly important if you intend to stay in Thailand for many years.

✅ If you want a deeper look at your options, including recommended providers and how to choose the right plan, you can explore my detailed health insurance guide for expats in Thailand.

📌 Choosing not to have insurance might lower your monthly expenses in the short term, but it also increases your exposure to unexpected costs.

Your Safety Buffer (The Number Most People Get Wrong)

One of the most common mistakes people make when planning their move to Thailand is focusing only on expected costs, while completely underestimating the importance of a financial safety buffer.

On paper, your budget might look sufficient. You’ve calculated your rent, daily expenses, and initial setup costs. But real life rarely follows a perfect plan, especially in a new country.

Unexpected situations can come up quickly, such as:

- delays in visa processing or changes in requirements

- difficulty finding suitable long-term accommodation

- higher-than-expected living costs in the first months

- medical issues or emergencies

- the need to travel unexpectedly

These are not rare scenarios. They are part of the reality of relocating.

📌 A safety buffer is what allows you to handle these situations without stress or having to make rushed decisions.

Recommended Buffer

As a general guideline, you should aim for:

✅ At least 3 to 6 months of living expenses as a financial buffer

For example:

- Basic living → 120,000 – 300,000 THB buffer

- Comfortable lifestyle → 150,000 – 500,000 THB buffer

📌 This is separate from your relocation budget and should ideally remain untouched unless genuinely needed.

In my experience, it’s not the planned expenses that cause problems. It’s the unexpected ones, combined with not having enough time to adapt. Having a buffer is not about being overly cautious. It’s about giving yourself time and flexibility to adjust, especially during the first few months when everything is still unfamiliar.

📍 Without it, even small issues can turn into unnecessary pressure.

Common Mistakes Expats Make

Even with good planning, it’s easy to misjudge the financial side of moving to Thailand. Most mistakes don’t come from lack of effort, but from assumptions that don’t match reality.

✅ Here are some of the most common ones:

Underestimating the First Few Months

The initial period after arrival is usually the most expensive.

Short-term accommodation, deposits, setup costs, and daily spending while you’re still figuring things out can push your expenses higher than expected.

📌 Many people budget for “normal life” from day one, but it takes time to reach that point.

Assuming Thailand Is Always Cheap

Thailand can be affordable, but it’s not as cheap as many people expect, especially if you want comfort and convenience.

Living in central areas, eating out regularly, or maintaining a Western lifestyle can quickly increase your monthly expenses.

📌 The idea of “living cheaply in Thailand” often doesn’t match how most expats actually live.

Ignoring Health Insurance

Some people delay getting health insurance to save money at the beginning.

While this reduces monthly costs in the short term, it also increases financial risk if something unexpected happens.

📌 One medical issue can easily outweigh months or even years of saved premiums.

Committing Too Quickly

Signing a long-term rental, buying a vehicle, or locking into a lifestyle too early can limit your flexibility.

It’s usually better to take your time, explore different areas, and understand your real needs before making longer-term commitments.

📌 Flexibility in the beginning often saves money later.

Not Having a Proper Buffer

This is one of the most common and most impactful mistakes.

Arriving with just enough money to cover expected costs leaves no room for adjustment. Even small unexpected expenses can create pressure and lead to poor decisions.

📌 A financial buffer is not optional if you want a smooth transition.

✅ Most of these mistakes are avoidable. With realistic expectations and a bit of planning, you can significantly reduce financial stress and make your move to Thailand much smoother.

Realistic Budget Scenarios

To make the numbers more concrete, it helps to look at a few realistic scenarios. These are not exact budgets, but they reflect how different lifestyles typically play out in Thailand.

Basic Living

This setup is focused on keeping costs under control while still maintaining a comfortable day-to-day life.

You might:

- live in a simple apartment or older condo

- eat mostly local food

- use public transport or a motorbike

- keep entertainment and travel modest

Typical monthly budget: 35,000 – 50,000 THB

📌 This approach works well for people who are flexible, don’t need luxury, and are comfortable adapting to a more local lifestyle.

Comfortable Expat Lifestyle

This is where most long-term expats find themselves.

You can expect:

- a modern condo in a decent location

- a mix of Thai and Western food

- regular use of taxis or Grab

- occasional travel and social activities

Typical monthly budget: 50,000 – 85,000 THB

📌 This level offers a good balance between comfort, convenience, and cost, without feeling restricted.

High Comfort / Western-Style Living

This lifestyle prioritizes comfort, convenience, and familiarity.

You might:

- live in a high-end condo or desirable location

- dine out frequently, including Western restaurants

- rely on taxis or private transport

- travel regularly and maintain an active social life

Typical monthly budget: 85,000 – 180,000+ THB

📌 At this level, you have fewer compromises, but costs can increase quickly depending on your choices.

✅ Where you fall within these ranges often depends less on Thailand and more on your personal habits and expectations. Most people don’t stay fixed in one category. Your lifestyle, priorities, and spending habits will likely evolve over time as you settle in and find your rhythm.

Estimate Your Personal Budget

The ranges and examples above give you a solid starting point, but your actual budget will depend on your personal situation, priorities, and plans.

Even small differences, like where you choose to live, how often you travel, or whether you include health insurance, can have a noticeable impact on your overall costs.

If you want to move beyond general estimates and calculate your own situation more accurately based on your own circumstances, you can use the relocation budget tool below.

✅ The tool allows you to adjust key factors such as lifestyle, location, and financial buffer to get a more realistic estimate tailored to your situation. Start with your situation below and adjust as needed.

Your Situation

Housing & Time Buffer

One-Time Setup Costs

Deposit + first rent is always included. Add any other likely setup costs below.

📌 Once you have a rough estimate, it becomes much easier to plan your move with confidence and avoid the common budgeting mistakes we discussed earlier.

💱 Currency Note:

All USD estimates are based on an approximate exchange rate of 1 USD = 35 THB.

Actual amounts may vary depending on current exchange rates.

Moving to Thailand doesn’t require a perfect financial plan, but it does require a realistic one.

The exact number you need will always depend on your lifestyle, expectations, and how much uncertainty you are willing to accept. What matters more is understanding where your money goes and giving yourself enough flexibility to adapt once you arrive.

In many cases, the move itself is not the difficult part. Adjusting to a new environment, finding your routine, and making decisions along the way is where financial pressure can build if your budget is too tight.

✅ If you approach it with a clear plan, a reasonable buffer, and realistic expectations, Thailand can offer a very comfortable and rewarding lifestyle.

From my experience, the people who enjoy living here the most are not the ones with the biggest budgets, but the ones who planned realistically and gave themselves room to adapt.

💬 If you’ve already gone through this process or are currently planning your move, feel free to share your thoughts or questions in the comments.